70 through 80 started with a recession, had an acute recession in the middle and ended in a recession:

Nonetheless we racked up impressive real growth for the decade. The 70s were not a good time but they beat this last decade all hollow.

I agree with you that 2007 started what was in effect a depression. I am very singular in that agreement, but I usually calculate from incomes rather than GDP, which makes me a rare bird indeed. I do it because it is highly accurate for years in the future. In 2002 I calculated a growth rate of 1.8% for the first decade.

However, calculating from income, which is far more accurate for projections, does imply a net real growth rate below 2.3% annually for the next decade. It is intractable. I have 2.1%. It might go to 2.3% if we continue to borrow more, or it might be 1.9%. But it will not be 2.5%.

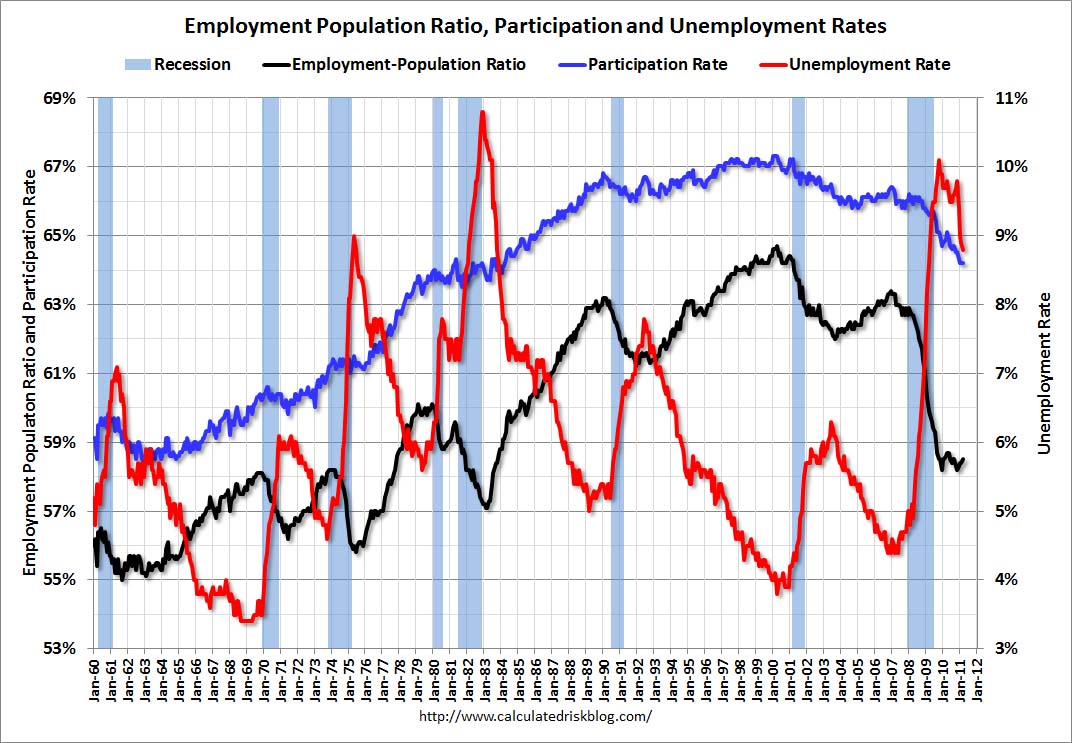

Further, the "jobless" recovery we all saw from 2001 is smack on the line for US recessions. As US production has dropped, jobless recoveries have become the norm. Each time we enter a downturn the recovery is slower.

We have been moving from one bubble to the next since the dot.com bubble of the 90s.

Further, there is a huge body of economic literature showing that a financial crisis such as the one we just endured (from fostering bubbles) has a very long time frame before economic recovery. You expect a decade; it takes that long to work your way out of it.

The US economy will slowly recover and regain strength by boosting production relative to consumption. But we are not going to boost production that quickly; consumption is going to fall to bring it back in line. We are going to raise taxes which will reduce consumption, and we are going to reduce social spending for the middle class, which will also reduce consumption.

Over time we will move back to a balanced economy, but we will not see 3% average growth for probably another 2 decades. This is not rare among OECD economies. As soon as you get your debt to the 90% level, your growth rate is doomed to slow significantly. There is a very large and empirically-based body of economic work on the function of debt and economies (high personal and high public debt are not that different in effect - we have both).

In part this is a function of demographics. Older people spend relatively little of their incomes on stuff and far more on basic needs. The 1990s change in SS/Medicare projections was due to several factors. The first was the change in CPI calculation, which reduced the growth of SS benefits quite significantly. The second was that the US birthrate rose.

In the US, personal incomes peak in the 50s and this has been true for a very long while. Due to our older population, we would expect to see US household income, on average, drop for over a decade. That has economic implications. The amount of private debt per household has very large implications for future consumption.

Consider student debt, which generally cannot be written off in bankruptcy. The amount of student debt we have racked up is frightening and should lower GDP about 1/2 a percentage point over the next decade at least. We could write it off, but that means the government assumes more debt, so it doesn't really disappear.