| Latest | Greatest | Lobby | Journals | Search | Options | Help | Login |

|

|

|

This topic is archived. |

| Home » Discuss » Archives » General Discussion: Presidential (Through Nov 2009) |

|

| CreekDog

|

Mon Mar-23-09 03:47 PM Original message |

| Is the main goal of the toxic asset plan to get the market to price the assets? |

| Printer Friendly | Permalink | | Top |

| ayeshahaqqiqa

|

Mon Mar-23-09 03:54 PM Response to Original message |

| 1. Your post is the first one that really explains what is happening |

| Printer Friendly | Permalink | | Top |

| CreekDog

|

Mon Mar-23-09 03:57 PM Response to Reply #1 |

| 2. and if the government priced the assets on its own, the market might not trust those decisions |

| Printer Friendly | Permalink | | Top |

| Beetwasher

|

Mon Mar-23-09 04:01 PM Response to Reply #2 |

| 5. FDIC Is Mediating The Process To Make Sure The Prices Are "Reasonable" |

| Printer Friendly | Permalink | | Top |

| ayeshahaqqiqa

|

Mon Mar-23-09 04:05 PM Response to Reply #2 |

| 7. Yep, Feds are making the market behave |

| Printer Friendly | Permalink | | Top |

| Tigermoose

|

Mon Mar-23-09 03:58 PM Response to Original message |

| 3. And Nationalization is not a magic bullet |

| Printer Friendly | Permalink | | Top |

| Political Heretic

|

Mon Mar-23-09 04:13 PM Response to Reply #3 |

| 12. No one is talking about that kind of nationalization |

| Printer Friendly | Permalink | | Top |

| Tigermoose

|

Mon Mar-23-09 04:24 PM Response to Reply #12 |

| 16. How do you define "solvent" vs "insolvent"? |

| Printer Friendly | Permalink | | Top |

| KittyWampus

|

Mon Mar-23-09 04:41 PM Response to Reply #16 |

| 20. solvent- not holding assets worth a fraction of what gamblers pretended they were worth |

| Printer Friendly | Permalink | | Top |

| Tigermoose

|

Mon Mar-23-09 04:46 PM Response to Reply #20 |

| 24. Here's an example I think that will make this clear. |

| Printer Friendly | Permalink | | Top |

| KittyWampus

|

Mon Mar-23-09 04:39 PM Response to Reply #3 |

| 19. so waving the magic "pretend these assets are worth something" wand is better? |

| Printer Friendly | Permalink | | Top |

| Beetwasher

|

Mon Mar-23-09 04:42 PM Response to Reply #19 |

| 21. The Assets ARE WORTH SOMETHING |

| Printer Friendly | Permalink | | Top |

| Political Heretic

|

Mon Mar-23-09 07:26 PM Response to Reply #21 |

| 29. Where's your statistic come from? |

| Printer Friendly | Permalink | | Top |

| Beetwasher

|

Mon Mar-23-09 09:35 PM Response to Reply #29 |

| 31. The National Avg Foreclosure Rate was Under 2% In 2008 |

| Printer Friendly | Permalink | | Top |

| EmilyAnne

|

Mon Mar-23-09 10:43 PM Response to Reply #19 |

| 37. Some are saying they are worthless, some are saying they are overvalued, some are saying that |

| Printer Friendly | Permalink | | Top |

| Thrill

|

Mon Mar-23-09 04:00 PM Response to Original message |

| 4. Let the Banks fail and you can kiss Obama's entire term away |

| Printer Friendly | Permalink | | Top |

| Rosa Luxemburg

|

Mon Mar-23-09 10:25 PM Response to Reply #4 |

| 34. I don't think the rest of the world's finance system would like that either |

| Printer Friendly | Permalink | | Top |

| CoffeeCat

|

Mon Mar-23-09 04:04 PM Response to Original message |

| 6. Ok my head hurts... |

| Printer Friendly | Permalink | | Top |

| CreekDog

|

Mon Mar-23-09 04:08 PM Response to Reply #6 |

| 9. it's the contamination that has left these assets with almost a zero price |

| Printer Friendly | Permalink | | Top |

| HamdenRice

|

Mon Mar-23-09 04:07 PM Response to Original message |

| 8. The main goal is someone holding them until they are properly valued |

| Printer Friendly | Permalink | | Top |

| CreekDog

|

Mon Mar-23-09 04:10 PM Response to Reply #8 |

| 10. but what if the hedge funds account for a significant portion of current market value? |

| Printer Friendly | Permalink | | Top |

| HamdenRice

|

Mon Mar-23-09 04:13 PM Response to Reply #10 |

| 13. Not sure I understand your question |

| Printer Friendly | Permalink | | Top |

| girl gone mad

|

Mon Mar-23-09 11:16 PM Response to Reply #10 |

| 43. By design, we are overpaying for the assets. |

| Printer Friendly | Permalink | | Top |

| Beetwasher

|

Mon Mar-23-09 04:19 PM Response to Reply #8 |

| 15. Your "Plan" Is Not Workable Or Pragmatic At This Point In Time |

| Printer Friendly | Permalink | | Top |

| HamdenRice

|

Mon Mar-23-09 05:07 PM Response to Reply #15 |

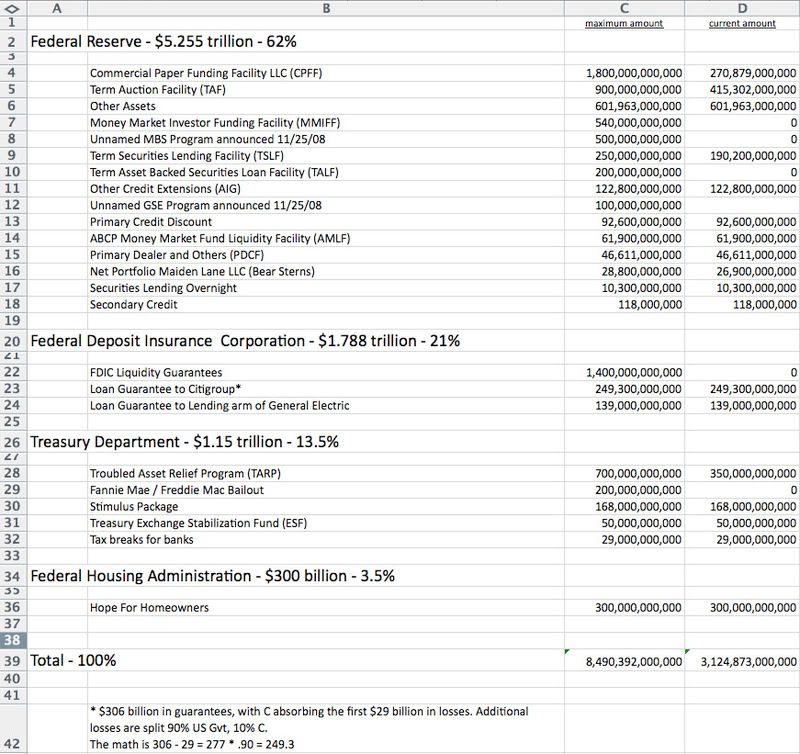

| 25. It's less work, more practical and the system is already in place. Check this graphic |

| Printer Friendly | Permalink | | Top |

| Beetwasher

|

Mon Mar-23-09 05:13 PM Response to Reply #25 |

| 26. No, It's Not In Place To Handle Assets On This Scale |

| Printer Friendly | Permalink | | Top |

| girl gone mad

|

Mon Mar-23-09 11:20 PM Response to Reply #26 |

| 46. Why not? |

| Printer Friendly | Permalink | | Top |

| Beetwasher

|

Tue Mar-24-09 09:06 AM Response to Reply #46 |

| 57. No They Don't, Not Right NOW |

| Printer Friendly | Permalink | | Top |

| Tigermoose

|

Mon Mar-23-09 04:36 PM Response to Reply #8 |

| 18. So what's your hangup? |

| Printer Friendly | Permalink | | Top |

| leftofthedial

|

Mon Mar-23-09 04:12 PM Response to Original message |

| 11. objective #1 is to socialize the risk |

| Printer Friendly | Permalink | | Top |

| Political Heretic

|

Mon Mar-23-09 04:14 PM Response to Reply #11 |

| 14. EXACTLY. Thank you for speaking the truth. |

| Printer Friendly | Permalink | | Top |

| Tigermoose

|

Mon Mar-23-09 04:26 PM Response to Reply #14 |

| 17. Yes. That's it exactly. Get over it. |

| Printer Friendly | Permalink | | Top |

| Political Heretic

|

Mon Mar-23-09 07:25 PM Response to Reply #17 |

| 28. That's just horse shit |

| Printer Friendly | Permalink | | Top |

| girl gone mad

|

Mon Mar-23-09 11:23 PM Response to Reply #17 |

| 48. The global banking collapse has already happened. |

| Printer Friendly | Permalink | | Top |

| amborin

|

Mon Mar-23-09 04:43 PM Response to Original message |

| 22. yes, & bad banks can bid up each other's bad asset prices--taxprs pay big $$ for worthless assets |

| Printer Friendly | Permalink | | Top |

| Beetwasher

|

Mon Mar-23-09 04:44 PM Response to Reply #22 |

| 23. Not W/ Government Money |

| Printer Friendly | Permalink | | Top |

| amborin

|

Mon Mar-23-09 06:47 PM Response to Reply #23 |

| 27. since large % of the assets are worthless, taxpayers will be paying lots for worthless assets |

| Printer Friendly | Permalink | | Top |

| Beetwasher

|

Mon Mar-23-09 09:01 PM Response to Reply #27 |

| 30. Please Post A Source For That Claim, It's Bullshit |

| Printer Friendly | Permalink | | Top |

| CreekDog

|

Mon Mar-23-09 10:16 PM Response to Reply #30 |

| 33. i don't even think the worst of them are worthless |

| Printer Friendly | Permalink | | Top |

| amborin

|

Mon Mar-23-09 11:17 PM Response to Reply #33 |

| 44. the collateral worth abt 50% of the mortgage? not in quite a few areas |

| Printer Friendly | Permalink | | Top |

| CreekDog

|

Mon Mar-23-09 11:30 PM Response to Reply #44 |

| 51. yes but that is not typical |

| Printer Friendly | Permalink | | Top |

| girl gone mad

|

Mon Mar-23-09 11:27 PM Response to Reply #33 |

| 49. Wait a second. |

| Printer Friendly | Permalink | | Top |

| amborin

|

Mon Mar-23-09 11:19 PM Response to Reply #30 |

| 45. & don't forget the real disaster looming: the commercial mortgages |

| Printer Friendly | Permalink | | Top |

| girl gone mad

|

Mon Mar-23-09 11:28 PM Response to Reply #45 |

| 50. yup. |

| Printer Friendly | Permalink | | Top |

| Beetwasher

|

Tue Mar-24-09 09:18 AM Response to Reply #45 |

| 58. You've Still Posted Not One Single Piece Of Data To Support That Bullshit |

| Printer Friendly | Permalink | | Top |

| EmilyAnne

|

Mon Mar-23-09 10:44 PM Response to Reply #27 |

| 38. How are they worthless? Do you mean just extremely overvalued, or do you actually think many of |

| Printer Friendly | Permalink | | Top |

| amborin

|

Mon Mar-23-09 11:37 PM Response to Reply #38 |

| 52. both but especially the latter |

| Printer Friendly | Permalink | | Top |

| EmilyAnne

|

Mon Mar-23-09 09:54 PM Response to Original message |

| 32. Here's a question that probably seems quite dumb. |

| Printer Friendly | Permalink | | Top |

| Honeycombe8

|

Mon Mar-23-09 10:35 PM Response to Original message |

| 35. No. It's to free the banks of those assets, and thereby free up their $$$ to loan. |

| Printer Friendly | Permalink | | Top |

| Honeycombe8

|

Mon Mar-23-09 10:38 PM Response to Original message |

| 36. The govt is not going to pay the same for those assets as investors, is my understanding. |

| Printer Friendly | Permalink | | Top |

| EmilyAnne

|

Mon Mar-23-09 10:46 PM Response to Reply #36 |

| 39. Which makes sense that they will need to be enticed to participate, even if they are assholes. |

| Printer Friendly | Permalink | | Top |

| Honeycombe8

|

Mon Mar-23-09 10:56 PM Response to Reply #39 |

| 41. I just made those numbers up as an example. What I heard on TV... |

| Printer Friendly | Permalink | | Top |

| EmilyAnne

|

Mon Mar-23-09 10:59 PM Response to Reply #41 |

| 42. I am sure it all breaks to give an advantage to the investors. That whole necessary evil thing. |

| Printer Friendly | Permalink | | Top |

| asphalt.jungle

|

Mon Mar-23-09 11:21 PM Response to Reply #41 |

| 47. was it this? |

| Printer Friendly | Permalink | | Top |

| Redbear

|

Mon Mar-23-09 10:47 PM Response to Original message |

| 40. But don't we already know what the market thinks they are worth, |

| Printer Friendly | Permalink | | Top |

| Kurt_and_Hunter

|

Mon Mar-23-09 11:38 PM Response to Reply #40 |

| 53. They'll participate because the plan is designed to over-pay |

| Printer Friendly | Permalink | | Top |

| EmilyAnne

|

Tue Mar-24-09 12:05 AM Response to Reply #53 |

| 55. Yikes! Everything was going so well until that last word! I got SCARED!! |

| Printer Friendly | Permalink | | Top |

| Gregorian

|

Mon Mar-23-09 11:41 PM Response to Original message |

| 54. My limited impression of this is that it is to avoid the alternative to doing nothing. |

| Printer Friendly | Permalink | | Top |

| EmilyAnne

|

Tue Mar-24-09 12:08 AM Response to Reply #54 |

| 56. Keep posting your thoughts. I think most of us are in the same boat. This is very confusing stuff |

| Printer Friendly | Permalink | | Top |

| DU

AdBot (1000+ posts) |

Thu Apr 25th 2024, 05:54 PM Response to Original message |

| Advertisements [?] |

| Top |

| Home » Discuss » Archives » General Discussion: Presidential (Through Nov 2009) |

|

Powered by DCForum+ Version 1.1 Copyright 1997-2002 DCScripts.com

Software has been extensively modified by the DU administrators

Important Notices: By participating on this discussion board, visitors agree to abide by the rules outlined on our Rules page. Messages posted on the Democratic Underground Discussion Forums are the opinions of the individuals who post them, and do not necessarily represent the opinions of Democratic Underground, LLC.

Home | Discussion Forums | Journals | Store | Donate

About DU | Contact Us | Privacy Policy

Got a message for Democratic Underground? Click here to send us a message.

© 2001 - 2011 Democratic Underground, LLC