Submitted by Tyler Durden on 11/10/2009 15:06 -0500

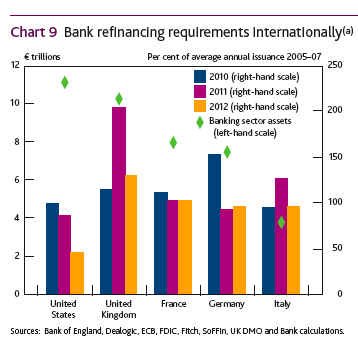

Zero Hedge recently highlighted the developing risk in the government's outstanding Treasury portfolio, where nearly 40% of all issues mature within the year. As such the roll risk for the US government is massive, and even the smallest unexpected macro blip would make the rolling/refinancing of roughly $5 trillion in debt very problematic. Yet the US government is not alone in this quandary of how to keep T-Bill interest rates at record lows: an earlier report by Moody's demonstrates that the banking system is in far, far worse shape: "we note that average maturities of new debt issuances rated by Moodys which we use as an indicator of general trends -- fell from 7.2 years to 4.7 years globally over the last five years. This is the shortest average maturity for new debt at any given point during the 30 years of bank funding history covered by our analysis. As a related matter, we estimate that banks that we rate will face maturing debt of about $10 trillion between now and the end of 2015, $7 trillion of which will occur by the end of 2012."

Let's do the math: the US Gov't needs to roll about $3 trillion (and increasing) every year, Commercial Real Estate has a $3 trillion refi cliff around 2014 and the banking system has a $7 trillion roll maturity by 2012. In other words at or about 2012, or at the time Barack Obama is sure to be enjoying record approval ratings (high or low, your choice) courtesy of 30% unemployment, the American economy will be straddled with not just the ongoing burden of issuing about $2 trillion in debt each year to finance what can only be characterized as a budget concocted by the most hard-core, raving lunatics in the Federal Insane Asylum Reserve, but will have to deal with roughly $15 trillion of rolling maturities.

http://www.zerohedge.com/article/us-lunatic-asylum-ie-economy-facing-approximately-15-trillion-roll-risk-2012