| Latest | Greatest | Lobby | Journals | Search | Options | Help | Login |

|

|

|

This topic is archived. |

| Home » Discuss » Latest Breaking News |

|

| ozymandius

|

Wed Feb-24-10 05:32 AM Original message |

| STOCK MARKET WATCH, Wednesday February 24 |

| Printer Friendly | Permalink | | Top |

| ozymandius

|

Wed Feb-24-10 05:36 AM Response to Original message |

| 1. Today's Reports |

| Printer Friendly | Permalink | | Top |

| UpInArms

|

Wed Feb-24-10 10:31 AM Response to Reply #1 |

| 44. U.S. Jan. new-home sales down 6.1% in past year - U.S. Jan. new-home sales drop 11% |

| Printer Friendly | Permalink | | Top |

| Roland99

|

Wed Feb-24-10 11:04 AM Response to Reply #44 |

| 47. New home sales hit record low in January |

| Printer Friendly | Permalink | | Top |

| ozymandius

|

Wed Feb-24-10 05:38 AM Response to Original message |

| 2. Oil hovers below $79 after US crude supply drop |

| Printer Friendly | Permalink | | Top |

| ozymandius

|

Wed Feb-24-10 05:41 AM Response to Original message |

| 3. Banks report small profit but 'problem' list jumps |

| Printer Friendly | Permalink | | Top |

| ozymandius

|

Wed Feb-24-10 05:43 AM Response to Original message |

| 4. Reid seeks extension of jobless aid |

| Printer Friendly | Permalink | | Top |

| ozymandius

|

Wed Feb-24-10 06:38 AM Response to Reply #4 |

| 13. Horrid Job Number Coming |

| Printer Friendly | Permalink | | Top |

| Robbien

|

Wed Feb-24-10 10:12 AM Response to Reply #4 |

| 42. Daily Job Cuts |

| Printer Friendly | Permalink | | Top |

| Juneboarder

|

Wed Feb-24-10 11:47 AM Response to Reply #42 |

| 57. OMG... that is just horrible! |

| Printer Friendly | Permalink | | Top |

| Loge23

|

Wed Feb-24-10 07:35 PM Response to Reply #42 |

| 77. Sears closing 20+ stores |

| Printer Friendly | Permalink | | Top |

| ozymandius

|

Wed Feb-24-10 05:46 AM Response to Original message |

| 5. Flagging confidence intensifies economic fears |

| Printer Friendly | Permalink | | Top |

| mbperrin

|

Wed Feb-24-10 08:33 AM Response to Reply #5 |

| 24. December 74 was the end of the semester before I graduated from college. |

| Printer Friendly | Permalink | | Top |

| stevebreeze

|

Wed Feb-24-10 08:51 AM Response to Reply #5 |

| 28. 74 was the first time I got laid off. |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Wed Feb-24-10 06:42 PM Response to Reply #5 |

| 69. 74 was the year of my 1st child, and pregnant with 2nd |

| Printer Friendly | Permalink | | Top |

| skoalyman

|

Wed Feb-24-10 11:28 PM Response to Reply #69 |

| 82. 74 was the year I was born |

| Printer Friendly | Permalink | | Top |

| ozymandius

|

Wed Feb-24-10 05:49 AM Response to Original message |

| 6. Facing pressure, Bernanke to address lawmakers |

| Printer Friendly | Permalink | | Top |

| ozymandius

|

Wed Feb-24-10 06:04 AM Response to Reply #6 |

| 7. Bernanke Likely to Face Questions on Jobless Recovery |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 06:07 AM Response to Original message |

| 8. People Are Starting to Pay Attention to The Economic Realities |

| Printer Friendly | Permalink | | Top |

| ozymandius

|

Wed Feb-24-10 06:27 AM Response to Reply #8 |

| 11. Good morning, Demeter and all. |

| Printer Friendly | Permalink | | Top |

| boomerbust

|

Wed Feb-24-10 06:49 AM Response to Reply #11 |

| 15. One event that comes to mind |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Wed Feb-24-10 07:46 AM Response to Reply #8 |

| 19. The desire to destroy |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 08:58 AM Response to Reply #19 |

| 31. Chilling. I'm Shivering As I Read Your Post |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Wed Feb-24-10 09:07 AM Response to Reply #31 |

| 33. Sunday -- and think about it |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 09:15 AM Response to Reply #33 |

| 35. I've Always Seen the Invisible Hand of Christianity in Govt. |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Wed Feb-24-10 09:33 AM Response to Reply #35 |

| 40. It's all co-optation |

| Printer Friendly | Permalink | | Top |

| Festivito

|

Wed Feb-24-10 06:08 AM Response to Original message |

| 9. Debt: 02/22/2010 12,403,027,179,655.21 (UP 972,344,066.53) (Mon) |

| Printer Friendly | Permalink | | Top |

| Festivito

|

Wed Feb-24-10 04:07 PM Response to Reply #9 |

| 65. Debt: 02/23/2010 12,409,374,679,862.09 (UP 6,347,500,206.88) (Tue) |

| Printer Friendly | Permalink | | Top |

| ozymandius

|

Wed Feb-24-10 06:18 AM Response to Original message |

| 10. Geithner May Give Regulators Leeway in Applying Volcker Rule |

| Printer Friendly | Permalink | | Top |

| ozymandius

|

Wed Feb-24-10 06:56 AM Response to Reply #10 |

| 16. Volcker Rule Being Deep Sixed |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Wed Feb-24-10 07:04 AM Response to Reply #16 |

| 17. Am I too cynical? |

| Printer Friendly | Permalink | | Top |

| Dr.Phool

|

Wed Feb-24-10 07:20 AM Response to Reply #17 |

| 18. It's sure starting to look like it. |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Wed Feb-24-10 07:51 AM Response to Reply #18 |

| 21. Congrats for your dad and for you |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Wed Feb-24-10 07:57 AM Response to Reply #18 |

| 22. My son in Ohio just got a contract on their house yesterday |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 08:42 AM Response to Reply #18 |

| 25. All my fingers crossed for you, Doc |

| Printer Friendly | Permalink | | Top |

| Ghost Dog

|

Wed Feb-24-10 08:15 AM Response to Reply #17 |

| 23. You're not (it's what I thought at the time). Meanwhile: TOBIN TAX moves: |

| Printer Friendly | Permalink | | Top |

| Dr.Phool

|

Wed Feb-24-10 02:14 PM Response to Reply #17 |

| 62. Too many questions. |

| Printer Friendly | Permalink | | Top |

| Roland99

|

Wed Feb-24-10 09:22 AM Response to Reply #16 |

| 37. Obama = The Geraldo Rivera Administration |

| Printer Friendly | Permalink | | Top |

| ozymandius

|

Wed Feb-24-10 06:35 AM Response to Original message |

| 12. Headline of the Day: Lending Falls at Epic Pace |

| Printer Friendly | Permalink | | Top |

| ozymandius

|

Wed Feb-24-10 06:44 AM Response to Original message |

| 14. Redux from Tuesday: Goldman Sachs Minted Most Toxic CDOs |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 08:45 AM Response to Reply #14 |

| 26. If Europe Can Take Down Goldman |

| Printer Friendly | Permalink | | Top |

| UpInArms

|

Wed Feb-24-10 07:51 AM Response to Original message |

| 20. dollar watch |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 08:47 AM Response to Reply #20 |

| 27. That Plaza Accord and the Louvre Accord that Was Supposed to Fix It |

| Printer Friendly | Permalink | | Top |

| UpInArms

|

Wed Feb-24-10 11:32 AM Response to Reply #27 |

| 55. then there was Basel I and II |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 08:51 AM Response to Original message |

| 29. Are Derivatives the Real Problem? |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 08:54 AM Response to Original message |

| 30. Judge approves BofA settlement with SEC |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 09:03 AM Response to Original message |

| 32. Greece threatens more than the euro By Gideon Rachman |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 09:07 AM Response to Original message |

| 34. Wells Fargo, You Never Knew What Hit You. |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 09:17 AM Response to Original message |

| 36. The Drive to Eliminate Social Security Accelerates By Shamus Cooke |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 09:24 AM Response to Original message |

| 38. How JP Morgan treats its clients: scandalously and in bad faith |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 09:31 AM Response to Reply #38 |

| 39. Does Judge Rakoff Smackdown of Heinous JP Morgan Conduct Mark Beginning of a Sea Change? |

| Printer Friendly | Permalink | | Top |

| Joe Chi Minh

|

Wed Feb-24-10 07:03 PM Response to Reply #39 |

| 70. That would be something. |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Wed Feb-24-10 09:39 AM Response to Original message |

| 41. Bullish a Year Ago, Robert Prechter Now Sees "the Biggest Bubble in History" |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Wed Feb-24-10 10:20 AM Response to Reply #41 |

| 43. Uncle Sam, er Uncle Ben and Cousin Timmeh have been protecting |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Wed Feb-24-10 02:22 PM Response to Reply #41 |

| 63. Deflation Is Coming and There's Nothing Bernanke Can Do About It, Says Robert Prechter |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Wed Feb-24-10 02:24 PM Response to Reply #41 |

| 64. Bear Market Armageddon: Why Prechter Might Be Right This Time |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 11:57 PM Response to Reply #64 |

| 84. Deflation: Caused By Money PilingUp in Hoards Instead of Circulating |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 10:46 AM Response to Original message |

| 45. A Prisoners Dilemma: AIG and Goldman Sachs Game Each Other And PwC |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 10:49 AM Response to Original message |

| 46. A Bit of Irony for Breakfast |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 11:08 AM Response to Original message |

| 48. Auerback/Wray: Memo to Greece: Make War, Not Love, With Goldman Sachs |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 11:13 AM Response to Original message |

| 49. The doomsday cycle Peter Boone Simon Johnson |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 11:19 AM Response to Original message |

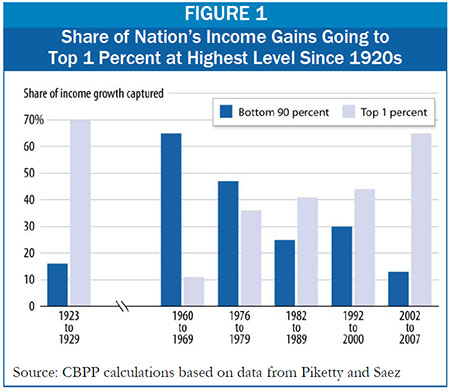

| 50. Wealth Disparities in U.S. Approaching 1920s Levels |

| Printer Friendly | Permalink | | Top |

| ozymandius

|

Wed Feb-24-10 09:15 PM Response to Reply #50 |

| 80. Let's not forget about debt levels. |

| Printer Friendly | Permalink | | Top |

| Roland99

|

Wed Feb-24-10 11:22 AM Response to Original message |

| 51. 11:21am - YAFPD!! |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 11:24 AM Response to Reply #51 |

| 52. Uncle Ben Must Have Said the Magic Word |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Wed Feb-24-10 11:27 AM Response to Reply #52 |

| 53. And Timmeh waved his magic. . . . . . |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 11:32 AM Response to Reply #53 |

| 54. I Truly Doubt He Has Anything to Wave--Be at Peace |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Wed Feb-24-10 11:45 AM Response to Reply #52 |

| 56. Yes, he said high unemployment and low inflation would mean low interest for a long long time... |

| Printer Friendly | Permalink | | Top |

| burf

|

Wed Feb-24-10 12:10 PM Response to Reply #51 |

| 58. One thing is for certain |

| Printer Friendly | Permalink | | Top |

| tclambert

|

Wed Feb-24-10 04:37 PM Response to Reply #58 |

| 66. We are working on genetically modified ponies that poop gold |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 06:28 PM Response to Reply #66 |

| 67. If I Mention that Michigan HAS NO Mountains, Are You Going to Kill Me? |

| Printer Friendly | Permalink | | Top |

| burf

|

Wed Feb-24-10 09:58 PM Response to Reply #67 |

| 81. I thought there were some up in th UP |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 11:50 PM Response to Reply #81 |

| 83. Barely Foothills |

| Printer Friendly | Permalink | | Top |

| Robbien

|

Wed Feb-24-10 12:58 PM Response to Original message |

| 59. Short Sale Rule Passes After 3-2 Party-Line Vote, Shorting Anything To Be Illegal Shortly |

| Printer Friendly | Permalink | | Top |

| Robbien

|

Wed Feb-24-10 01:29 PM Response to Original message |

| 60. Hedge Fund, P.E.-Backed Bank Buys Another Failed Bank |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Wed Feb-24-10 06:33 PM Response to Reply #60 |

| 68. That was just last Friday. Good Catch |

| Printer Friendly | Permalink | | Top |

| Roland99

|

Wed Feb-24-10 02:11 PM Response to Original message |

| 61. Yet another reason to loathe the auto industry (Chrysler/Dodge in particular) |

| Printer Friendly | Permalink | | Top |

| citizen snips

|

Wed Feb-24-10 07:21 PM Response to Original message |

| 71. Dollar May Extend Fall on Prospects Fed Will Keep Rates Low |

| Printer Friendly | Permalink | | Top |

| citizen snips

|

Wed Feb-24-10 07:23 PM Response to Original message |

| 72. S.E.C. Restricts Short-Selling and Addresses a Global Accounting Shift |

| Printer Friendly | Permalink | | Top |

| citizen snips

|

Wed Feb-24-10 07:28 PM Response to Original message |

| 73. The Plan on Fannie, Freddie to Come Next Year, Geithner Says |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Feb-25-10 12:00 AM Response to Reply #73 |

| 85. Gods Help Us; They've Got a Plan |

| Printer Friendly | Permalink | | Top |

| citizen snips

|

Wed Feb-24-10 07:30 PM Response to Original message |

| 74. Blockbuster to Close 500 or More U.S. Stores, Restructure Debt |

| Printer Friendly | Permalink | | Top |

| citizen snips

|

Wed Feb-24-10 07:32 PM Response to Original message |

| 75. Heating oil, gas up slightly as storms hit |

| Printer Friendly | Permalink | | Top |

| citizen snips

|

Wed Feb-24-10 07:34 PM Response to Original message |

| 76. Sector Snap: Newspaper shares rise on profits |

| Printer Friendly | Permalink | | Top |

| citizen snips

|

Wed Feb-24-10 07:36 PM Response to Original message |

| 78. Blockbuster posts 4Q loss of $435M as woes deepen |

| Printer Friendly | Permalink | | Top |

| citizen snips

|

Wed Feb-24-10 07:41 PM Response to Original message |

| 79. Treasurys surrender some gains after auction of 5-year notes |

| Printer Friendly | Permalink | | Top |

| DU

AdBot (1000+ posts) |

Thu Apr 25th 2024, 06:29 PM Response to Original message |

| Advertisements [?] |

| Top |

| Home » Discuss » Latest Breaking News |

|

Powered by DCForum+ Version 1.1 Copyright 1997-2002 DCScripts.com

Software has been extensively modified by the DU administrators

Important Notices: By participating on this discussion board, visitors agree to abide by the rules outlined on our Rules page. Messages posted on the Democratic Underground Discussion Forums are the opinions of the individuals who post them, and do not necessarily represent the opinions of Democratic Underground, LLC.

Home | Discussion Forums | Journals | Store | Donate

About DU | Contact Us | Privacy Policy

Got a message for Democratic Underground? Click here to send us a message.

© 2001 - 2011 Democratic Underground, LLC