| Latest | Greatest | Lobby | Journals | Search | Options | Help | Login |

|

|

|

This topic is archived. |

| Home » Discuss » Archives » General Discussion (01/01/06 through 01/22/2007) |

|

| TexasLawyer

|

Fri May-12-06 06:36 PM Original message |

| Home Foreclosures Up (63%!!!) As Mortgage Rates Climb |

| Printer Friendly | Permalink | | Top |

| Maine-ah

|

Fri May-12-06 06:37 PM Response to Original message |

| 1. kick. |

| Printer Friendly | Permalink | | Top |

| NoAmericanTaliban

|

Fri May-12-06 06:45 PM Response to Original message |

| 2. Now you know why they passed those bankruptcy laws |

| Printer Friendly | Permalink | | Top |

| henslee

|

Fri May-12-06 10:07 PM Response to Reply #2 |

| 16. What's next, debtors prison? |

| Printer Friendly | Permalink | | Top |

| TexasLawyer

|

Fri May-12-06 06:47 PM Response to Original message |

| 3. Lots of anecdotal information out there of a BIG problem brewing |

| Printer Friendly | Permalink | | Top |

| TexasLawyer

|

Fri May-12-06 06:50 PM Response to Original message |

| 4. Hey red states-- Georgia leads the nation in foreclosures |

| Printer Friendly | Permalink | | Top |

| TexasLawyer

|

Fri May-12-06 06:57 PM Response to Original message |

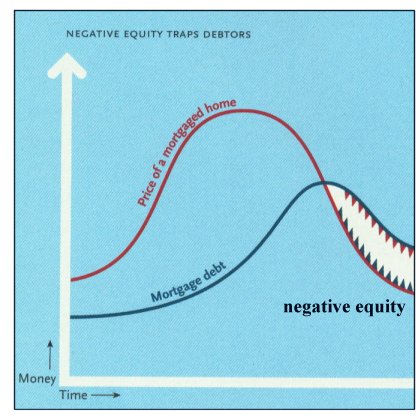

| 5. and get ready for negative equity |

| Printer Friendly | Permalink | | Top |

| cliss

|

Fri May-12-06 07:29 PM Response to Reply #5 |

| 10. Thanks for the info, TL. |

| Printer Friendly | Permalink | | Top |

| Tactical Progressive

|

Fri May-12-06 06:58 PM Response to Original message |

| 6. Those numbers are ridiculous |

| Printer Friendly | Permalink | | Top |

| Jack Rabbit

|

Fri May-12-06 06:59 PM Response to Original message |

| 7. But, but, but, the economy is just great |

| Printer Friendly | Permalink | | Top |

| TheCowsCameHome

|

Fri May-12-06 07:04 PM Response to Original message |

| 8. Gosh. Who would have predicted this happening? Incredible. |

| Printer Friendly | Permalink | | Top |

| VOX

|

Fri May-12-06 07:14 PM Response to Original message |

| 9. And all those folks who got sucked into interest-only mortgages... |

| Printer Friendly | Permalink | | Top |

| Warpy

|

Fri May-12-06 07:52 PM Response to Reply #9 |

| 11. I predicted it TEN years ago |

| Printer Friendly | Permalink | | Top |

| phylny

|

Fri May-12-06 08:38 PM Response to Original message |

| 12. I am not surprised. A client's husband worked for Fannie Mae and |

| Printer Friendly | Permalink | | Top |

| upi402

|

Fri May-12-06 09:03 PM Response to Original message |

| 13. My home is for sale, but friends tell me I'm too paranoid |

| Printer Friendly | Permalink | | Top |

| girl gone mad

|

Sat May-13-06 12:02 AM Response to Reply #13 |

| 19. I think inflation will.. |

| Printer Friendly | Permalink | | Top |

| upi402

|

Sat May-13-06 12:11 AM Response to Reply #19 |

| 20. Good point about materials costs, also |

| Printer Friendly | Permalink | | Top |

| NorthernSpy

|

Fri May-12-06 09:06 PM Response to Original message |

| 14. where will they go? |

| Printer Friendly | Permalink | | Top |

| upi402

|

Fri May-12-06 11:46 PM Response to Reply #14 |

| 17. Many who go to a mtg. counselor keep the house or sell in time |

| Printer Friendly | Permalink | | Top |

| TexasLawyer

|

Sat May-13-06 01:31 AM Response to Reply #14 |

| 21. negative equity |

| Printer Friendly | Permalink | | Top |

| Supersedeas

|

Fri May-12-06 10:00 PM Response to Original message |

| 15. but but but Tony Snowjob said that M$M are ignoring the Good news |

| Printer Friendly | Permalink | | Top |

| upi402

|

Fri May-12-06 11:59 PM Response to Reply #15 |

| 18. LOL-really! In my market it's 99% cheerleading |

| Printer Friendly | Permalink | | Top |

| TexasLawyer

|

Sat May-13-06 01:49 AM Response to Original message |

| 22. The nature of economic bubbles |

| Printer Friendly | Permalink | | Top |

| DU

AdBot (1000+ posts) |

Fri Apr 19th 2024, 02:28 AM Response to Original message |

| Advertisements [?] |

| Top |

| Home » Discuss » Archives » General Discussion (01/01/06 through 01/22/2007) |

|

Powered by DCForum+ Version 1.1 Copyright 1997-2002 DCScripts.com

Software has been extensively modified by the DU administrators

Important Notices: By participating on this discussion board, visitors agree to abide by the rules outlined on our Rules page. Messages posted on the Democratic Underground Discussion Forums are the opinions of the individuals who post them, and do not necessarily represent the opinions of Democratic Underground, LLC.

Home | Discussion Forums | Journals | Store | Donate

About DU | Contact Us | Privacy Policy

Got a message for Democratic Underground? Click here to send us a message.

© 2001 - 2011 Democratic Underground, LLC